How to Choose the Right Advisory Team for your Farm

Read More

Financial planning is an important component of a successful farming operation, especially in a state like Iowa, where agriculture serves as the backbone of the economy. Effective financial management enables farmers to navigate market fluctuations, manage debt responsibly and make strategic investments contributing to long-term profitability. Given the capital-intensive nature of farming, proper budgeting cash flow management and loan structuring are essential for sustainability.

Iowa’s agricultural landscape presents both unique challenges and opportunities. Farmers in the state benefit from highly productive soil, access to robust commodity markets and supportive agricultural programs. However, they also face unpredictable weather patterns, fluctuating commodity prices, rising input costs and evolving regulations that can impact profitability. Managing these factors requires strategic financial planning, risk mitigation and a strong understanding of available funding options.

The purpose of this guide is to help Iowa farmers optimize their financial health and ensure long-term sustainability. By providing insights into farm loans, debt management strategies and key financial considerations, this resource aims to equip farmers with the knowledge needed to make informed decisions, secure stable financing and enhance the resilience of their agricultural operations.

Farm financial planning is the process of assessing, organizing and managing financial resources to ensure the long-term success and sustainability of a farming operation. It involves a combination of budgeting, cash flow management, debt management, tax planning and investment strategies. The key components of financial planning for farms include:

Financial planning is essential for Iowa farmers because agriculture is a capital-intensive industry with numerous uncertainties. A well-structured financial plan allows farmers to:

Iowa farmers encounter several financial challenges that can impact their profitability and sustainability:

By understanding these challenges and implementing a strategic financial plan, Iowa farmers can enhance their resilience and position their farms for long-term success.

Budgeting and Cash Flow Management for Farmers

Financial stability is essential for farmers to navigate seasonal fluctuations, manage operating costs and ensure long-term profitability. Proper budgeting and cash flow management help farmers anticipate financial challenges, allocate resources efficiently and make strategic decisions.

Importance of Tracking Income and Expenses

Farmers operate in a highly variable environment where income depends on market conditions, weather and yield outcomes. Tracking income and expenses helps in:

Tools and Templates for Farm Budgeting

Farmers can use various tools and templates to streamline budgeting and cash flow management:

By implementing structured budgeting practices and using appropriate tools, farmers can improve financial decision-making, optimize cash flow and enhance the overall efficiency of their operations.

Accurate and organized record keeping is essential for the success of any farm operation. It provides valuable insights into the farm’s financial performance, helps with decision-making, and is crucial for tax preparation and compliance. Here’s a breakdown of best practices and legal considerations for Iowa farmers:

Through these services, we aim to empower farmers with the knowledge, tools and strategies necessary to manage their finances effectively, optimize profitability and ensure the long-term sustainability of their farms. Integrating budgeting and cash flow management into your overall farm business planning can create a robust foundation for financial success.

Farming is inherently risky. Iowa farmers face a multitude of potential challenges, from unpredictable weather and fluctuating markets to pest infestations and equipment breakdowns. Effective risk management is crucial for ensuring the long-term viability of a farm operation. Here’s a look at some key strategies:

Crop Insurance Options in Iowa:

Crop insurance is a cornerstone of risk management for Iowa farmers. It helps protect against financial losses due to covered perils. Several options are available:

The structure of farm operations plays a key role in risk management. Important considerations include:

A plan should encompass an understanding of available marketing tools, including cash tools for immediate sales, futures contracts for setting sale prices and options contracts to provide flexibility and protect against price drops. Integration of these tools with broader financial analysis—combining insights from market fundamentals, technical analysis and regular profit and loss assessment ensures decisions are made with a comprehensive view of their potential impact. This should include how various types of agricultural insurance can buffer financial losses from poor yields or market downturns.

To mitigate risks effectively, farmers should engage in regular market analysis to stay informed about trends and be prepared to adjust strategies quickly.

It is important to know your cost of production and understand your breakeven points. This knowledge allows for more grounded decision-making, focusing on securing profit rather than chasing the highest possible price. Selling a portion of your product at a profit, when market conditions are favorable, can ensure financial stability and reduce risk exposure.

Diversifying both crop types and income sources can significantly reduce the risk of failure. Planting a variety of crops protects against the total loss of production due to disease or adverse weather. Additionally, exploring alternative income streams such as agritourism or organic production can provide financial stability when traditional crops underperform.

The use of drought-resistant varieties, advanced irrigation systems and precision agriculture techniques like soil moisture sensors enhance crop resilience and operational efficiency. Tools like AgriBuilder from Adams Brown amplify these benefits by integrating elements of farm management, such as financial monitoring and resource management. This not only optimizes resource use but also improves decision-making, making farms more efficient and less prone to risks.

Farmers, particularly those running small to medium-sized operations, have always shown adaptability and ingenuity in the face of challenges. Among these challenges, ransomware attacks on computer systems have emerged as a predominant threat. Such attacks not only halt production but can also lead to significant financial losses, underscoring the need for robust security measures.

While small to medium-sized farms might perceive themselves as unlikely targets, the reality is that cybercriminals are casting wide nets, indiscriminately ensnaring whoever falls within their reach. It’s a reminder that in today’s interconnected environment, no operation is too small to be considered at risk.

Ransomware attacks, where malicious software encrypts files on a device or network until a ransom is paid, have become alarmingly common. For farmers, an attack can mean the loss of critical data, from operational records to financial information, crippling their ability to work and manage their farms effectively. Such incidents not only result in immediate financial strain but also pose long-term challenges in restoring operations and regaining lost data.

Strategies for Farmers to Protect Against Ransomware

Farmers must be proactive in adopting cybersecurity measures, seek collaborative solutions and advocate for supportive practices that enhance the resilience of the agricultural sector against cyber threats.

By combining these strategies, Iowa farmers can create a comprehensive risk management plan that helps them navigate the challenges of agriculture and ensures the long-term success of their farm operation. Regularly reviewing and updating this plan is essential to adapt to changing conditions and new risks.

The agricultural sector is increasingly targeted by cybercriminals due to its reliance on digital tools, IoT devices and interconnected systems. These vulnerabilities pose significant risks to financial stability, operational continuity and supply chain integrity. Below are the most common cyber threats affecting agriculture:

Phishing schemes involve deceptive emails or messages designed to steal login credentials, financial information or sensitive data. These attacks often impersonate suppliers, government agencies or banks, tricking farmers or employees into clicking malicious links or sharing personal information. For instance, phishing can lead to unauthorized access to financial accounts, data theft or fraudulent transactions.

Ransomware attacks involve malware that locks access to essential systems or data until a ransom is paid. In agriculture, ransomware can disrupt critical systems like farm management software or IoT devices, halting operations. For example, in 2021, Iowa-based NEW Cooperative was hit with a $5.9 million ransom demand, threatening to disrupt grain and livestock supply chains. These attacks can cause significant downtime, operational delays and financial losses.

Data breaches expose sensitive farm data, such as supplier contracts, financial records, crop schedules and proprietary technologies. Breached data can be sold on the dark web or exploited for financial gain. A 2020 report noted a 600% increase in data breaches targeting U.S. agriculture companies, reflecting the sector’s growing vulnerability.

The increasing use of IoT devices, such as automated irrigation systems, drones and GPS-enabled equipment, creates new attack surfaces. Many IoT devices lack robust security measures, making them susceptible to unauthorized access. Cybercriminals can exploit these vulnerabilities to disrupt operations, alter farming schedules or access connected systems.

Supply chain attacks target interconnected systems within the agricultural industry, including distributors, equipment suppliers and logistics providers. A breach in one part of the supply chain can cascade through the entire network, causing delays, financial losses and reputational damage.

Malware and spyware infect devices with stealing information, monitor activity or disrupt systems. These threats can compromise farm management software, exposing sensitive data or interfering with daily operations.

Social engineering attacks manipulate individuals into divulging confidential information or granting unauthorized access. These attacks exploit human error, often through phone calls or fake correspondence, to breach farm systems or accounts.

State agricultural programs and financial assistance

Iowa’s agricultural economy is a cornerstone of the state’s identity, contributing significantly to both the national and global food supply. To support this critical sector, Iowa offers a variety of programs through the Iowa Department of Agriculture and Land Stewardship (IDALS) and other state agencies. These programs focus on financial assistance, conservation, risk management and support for beginning farmers, all aimed at fostering sustainable agricultural practices and economic resilience.

The state’s climate and soil conditions exert a profound influence on the financial decisions of its farmers.

Climate Variability

Iowa’s agricultural sector faces significant challenges from its variable climate. Droughts, floods and extreme temperatures are frequent occurrences, posing substantial risks to crop yields.

Soil Diversity and Challenges

Iowa boasts diverse soil types, ranging from highly fertile loess soils to less productive areas.

Financial Implications

Iowa’s climate and soil conditions significantly influence the financial decisions of its farmers. By understanding these factors and implementing appropriate adaptation strategies, farmers can enhance their resilience, improve profitability and ensure the long-term sustainability of their operations.

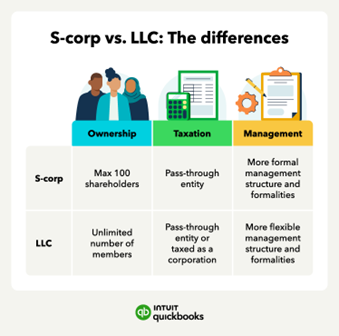

When it comes to deciding on an entity structure, farm owners should ask themselves:

Special Considerations for C Corporations Electing S Corporation Status

A C Corporation electing S Corporation status must be mindful of the built-in gains tax over a five-year period. This tax applies if assets are sold at a gain that was present at the time of the S election. Additionally, all shareholders must qualify under S Corporation requirements.

The benefits of electing S Corporation status include eligibility for the Qualified Business Income deduction and favorable long-term capital gains tax rates on real estate and other investments, which are not available under traditional C Corporation treatment. Despite the switch in taxation, the legal structure remains intact, providing ongoing corporate protection.

Tax Reporting & Trust Considerations

C Corporations file taxes using Form 1120, whereas S Corporations and other pass-through entities use different forms that reflect individual income reporting. On the topic of succession planning, while a revocable trust offers flexibility akin to a will, an irrevocable trust serves a distinct purpose, providing a more permanent solution for asset protection and tax planning.

Changing Entity Structures

As a farm evolves, so too might its needs for liability protection and tax management. For instance, shifting from a sole proprietorship to an LLC can provide necessary asset protection as the business grows. Adjustments in the tax landscape or a change in the farm’s financial strategy might also prompt a shift, like moving from a C Corporation to an S Corporation to take advantage of more favorable tax treatments for pass-through income.

Back in the day, but not all that long ago, farmers inherited farms from their parents. These transfers happen today, too, but come with numerous business challenges and implications. If you are considering passing your farm to the next generation, also known as succession planning, it’s important to be aware of potential pitfalls to make the transition as smooth as possible.

As the saying goes, “Failing to plan is planning to fail.” Those who are 65 and haven’t started this process are already behind the 8-ball. You must start early! Succession planning across all industries takes a lot of time, but agriculture has its own complexities to consider. Most farmers with large, successful operations don’t have a lot of cash on hand. Cash is often rolled back into the farm, impacting cash flow. Farms typically also have more equity tied up in assets than in other industries. These characteristics mean that more time is necessary to plan and execute a successful transition of ownership.

Starting the succession planning process late can make it impossible for your farm to continue after you pass away. Ideally, start the process in your early-to-mid-40s, especially if your children are approaching college age. Not only must you start early, but you need to know your future goals for your family and the continuation of your farm.

Part of starting early means getting the house in order, so to speak. It’s common for the next-generation of farmers to stick around to help mom and dad grow the farm but not grow themselves. This means that when the farm is ultimately transitioned, one challenge the next generation may face is getting a leverage model in place. Significant benefits to the management of your farm can come from the next generation obtaining off-the-farm education, training and skills.

Your setup of ownership, processes, procedures and overall operations can be greatly beneficial, but can also cause issues. In a multi-generation farm, one of the grandkids might look around and say, “Grandpa owns everything; Dad doesn’t own anything yet; I’m not sticking around because there’s nothing here for me.”

Structuring your legal entities can make navigating family dynamics much easier. Even if you haven’t solidified every detail like retirement, who is managing which aspects, etc., leveraging the right structure early on enables you to make quicker and more effective decisions.

A good business practice that goes hand-in-hand with succession planning is having a will and a trust. Wills are designed to protect your family, your farm, and other core assets while outlining exactly what should happen after your passing. Trusts are designed to provide you and your family with legal protection for your (the trustor’s) assets and to ensure the proper distribution of these assets based on your wishes. Trusts can also be a vehicle to avoid probate at your death, which can have very large estate tax implications and savings.

The bottom line is you should have a will and a trust. Having these tools in place can mean the difference between your farm flourishing or withering when life-altering events occur. If you don’t have these tools, put a will and a trust at the top of your priority list. If you have a will or trust, but haven’t updated either in a long time, revisit the documents and update as appropriate.

According to the IRS, the estate tax is a tax on your right to transfer property at your death. When it comes to estate planning, there is a common notion that time will always be on our side. However, as the sun begins to set on 2025, a unique and golden opportunity for the tax-efficient transfer of wealth is also fading. This circumstance is rendered even more critical with the ongoing market volatility, marking an opportune moment to optimize taxable estates before the market returns back to normalcy.

Some farmers struggle to manage their farm like a true business. Because of the market and price volatility in our economics today, part of this switch includes monitoring costs and knowing your break even.

For example, when you plant wheat, it might be selling for $7.50. But when you harvest, it might be selling for $6.20, but you needed to sell for $6.65 to break even. Opportunities to lock in high prices through active marketing are out there. You must know the selling price you need to break even and account where you can make a profit.

Depending solely on a single crop or livestock might prove detrimental. Embrace diversification by venturing into different crops, integrating crop-livestock systems or exploring agritourism. Additionally, secure insurance policies for potential risks like drought, pest infestations or market downturns.

Debt Management and Farm Loans

Effective debt management is crucial for farmers to maintain financial stability and ensure the long-term success of their operations. Understanding the types of agricultural loans available, strategies for managing debt, and the implications of interest rates and repayment terms can help farmers make informed financial decisions.

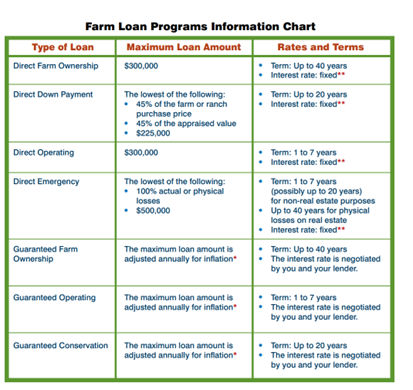

In Iowa, farmers have access to various loan options tailored to meet their specific needs:

Beginning Farmer Loan Programs: The Iowa Finance Authority’s Beginning Farmer Loan Program assists new farmers in acquiring agricultural property by offering loans at reduced interest rates, typically 20-25% below prevailing market rates. This program can be used to purchase agricultural land, machinery, equipment, breeding livestock or buildings.

How to Manage Debt Effectively

Effective debt management involves several strategies:

Understanding Interest Rates and Repayment Terms

A clear understanding of interest rates and repayment terms is vital:

By understanding these elements, farmers can structure their debt in a way that aligns with their financial capabilities and operational timelines, ensuring sustainable financial management.

Each year’s tax plan should be in alignment with your long-term strategic plan and vision for the success of your farm as well as personally. Showing a profit and paying taxes each year can be important for farmers because it allows them to take advantage of government incentives and tax breaks. Here are some of the fundamental tax planning tools for farmers:

These are just a few of the planning options to consider. Tax planning requires creative thinking and a strong understanding of the tax code. Currently, the tax code recognizes the difficult environment that farmers face and allows CPAs to use various tools to manage taxable farm income annually.

Farmers and agricultural businesses can take advantage of various tax deductions and credits to reduce their tax liability and improve financial efficiency. Below are key deductions and credits available to those in the agriculture sector.

There are many tax credits available to Iowa farmers designed to help reduce taxable income for a variety of qualifying activities, including:

The R&D tax credit is designed to encourage businesses, including farms, to invest in research and development activities. For row crop producers, this means that efforts to develop or improve products, processes or software can qualify. The key criteria for these activities are that they involve a process of experimentation aimed at discovering new or improved functionalities.

Here are some examples of activities that have qualified for the R&D tax credit in the past:

The financial impact of the R&D tax credit can be significant. For row crop producers, the potential to lower tax liability can range from $20,000 to $300,000, depending on the extent of qualifying research activities. These savings can be reinvested into your operation to further enhance productivity and profitability.

Understanding and applying for the R&D tax credit can seem daunting. Many farmers are unsure if their activities qualify or how to document them properly. This is where partnering with experienced advisors can make a difference. At Adams Brown, we specialize in helping row crop producers navigate the complexities of the R&D tax credit. Our experts will work with you to evaluate your activities, ensure they meet the necessary criteria and guide you through the application process.

Here’s a comprehensive list of resources for Iowa farmers, covering government agencies, local cooperatives, farming associations and educational programs:

Farm financial management is the process of planning, monitoring and controlling financial resources in agricultural operations to maximize profitability, manage risks and ensure long-term sustainability. It includes activities such as budgeting, cash flow management, investment planning, and financial analysis.

Financial management is important for farmers because it helps them make informed decisions, allocate resources efficiently, manage debt responsibly, and maintain financial stability during market fluctuations. Proper financial management also aids in tax planning and securing financing for future growth.

Farmers should maintain three primary financial statements:

Farmers can create an effective budget by estimating projected income from crop and livestock sales, government payments and other revenue sources. They should also account for fixed costs such as land payments, equipment loans, and insurance, as well as variable costs like seeds, feed and labor. Including a contingency fund for unexpected expenses can help maintain financial stability.

Farmers can manage cash flow effectively by tracking income and expenses regularly, aligning loan payments with income cycles, using short-term financing for seasonal needs, and maintaining cash reserves for emergencies. A well-managed cash flow ensures that the farm can meet financial obligations and continue operating smoothly.

Farmers can use a variety of financial tools, including accounting software such as QuickBooks, FarmBooks and Granular, to track income and expenses. Spreadsheets can also be used for budgeting and financial planning, while specialized agricultural financial tools like FINPACK provide advanced analysis and forecasting.

Farmers can reduce financial risk by diversifying their operations to include multiple crops or livestock, purchasing crop insurance to protect against weather and market fluctuations, managing debt carefully to avoid excessive borrowing, and implementing marketing strategies such as futures contracts or cooperative agreements.

Common financial mistakes that farmers should avoid include failing to maintain up-to-date financial records, overextending credit or taking on excessive debt, neglecting to budget for equipment repairs and capital improvements, and overlooking risk management options such as insurance and diversification.

Farmers can finance new equipment and farm expansion through traditional bank loans, which are often secured by farm assets, USDA loan programs designed to support agricultural businesses, and leasing options that provide lower upfront costs for machinery. Exploring grant opportunities and cooperative financing programs can also provide additional funding sources.

Farm succession planning can be integrated into financial management by establishing a structured business entity such as an LLC or partnership, developing a transition plan for future generations or new owners, and using estate planning tools to minimize tax liabilities. Consulting financial and legal professionals can help ensure a smooth transition and long-term financial stability for the farm.

As an owner or manager of an agribusiness, you are tasked with navigating various challenges that extend beyond the basics of accounting and wealth management. Effective forecasting, management and strategic planning are important to your success. You’ll need to tackle issues such as responding adeptly to market volatility, addressing labor shortages and planning for generational transitions in leadership. Each of these obstacles requires a careful strategy to ensure your financial objectives are achieved, securing the sustainability and growth of your business.

Family farms and corporate entities involved in many different types of crop production (farming and contract farming), as well as businesses focused on agrichemicals, breeding, distribution, farm machinery, processing, seed supply and marketing and retail sales are among those we help.

Adams Brown offers assistance with the following accounting services:

Complete the form to the right to start a conversation with our agriculture team.