How AI & Tariffs are Changing the Way Companies are Valued

Read More

A business valuation is the process of determining the economic value of a company, using standardized methods to assess what the business is worth in the current market. For business owners, a valuation is more than just a number—it’s a crucial financial tool that supports smarter planning, growth and decision-making. Knowing your company’s value provides the clarity and confidence needed to navigate those transitions effectively, whether you’re considering a sale, succession plan or investor relationship.

Owners typically seek valuations during key milestones such as preparing to sell the business, bringing in new partners, resolving disputes, applying for financing or fulfilling estate and gift tax requirements. In each case, an accurate valuation ensures that stakeholders are makingmake decisions based on objective financial realities rather than guesswork or emotion.

A well-prepared valuation can shape negotiations, influence deal terms and uncover value drivers that owners may not have considered. It can also help identify operational risks, inefficiencies or revenue opportunities allowing for strategic course corrections before major transactions take place. Ultimately, understanding the value of your business empowers you to protect, grow and eventually exit your company on your own terms.

As a business owner, you’re intimately acquainted with many facets of your company –, from day-to-day operations to long-term goals. However, one crucial aspect often gets overlooked: the actual value of your business. And no, it’s not just about a number or a price tag. Understanding the true worth of your business is like holding a mirror up to your company, revealing its strengths, potential risks and opportunities for growth.

Valuations play a crucial role in specific scenarios, such as assessing the value of a business in an estate planning context. However, they can also aid in guiding management decisions and informing the management team when setting goals and developing a strategic plan. It’s important to understand the various contexts to determine the most suitable time for conducting a valuation.

Primary Drivers for Business Valuation

The income approach is a way of determining the value of a business by converting anticipated economic performance into a present value.

Put another way, the value of a business is related to the present value of all future cash flows that the business is reasonably expected to produce. Therefore, estimates of future cash flows, and an appropriate discount rate, are key components of the income approach.

As part of the income approach, the capitalization of cash flow method is applied when a company’s growth and earnings have stabilized. This method can be applied to a mature company that is not going through a growth cycle, and for which operations are expected to continue in the future as they have in the past.

This method is a preferred method for most business appraisers and business brokers given its simplicity. However, small changes to the inputs can lead to a wide disparity in value. Business appraisers need to support the inputs substantially, given many risk and growth factors.

Normalizing adjustments are part of the business valuation process for nearly every company. These are adjustments that are made to ensure that the final valuation reflects “normal” operating performance, absent the unusual non-recurring income and expenses that most companies have from time to time. These may include a one-time gain from the sale of an asset, an insurance settlement or restructuring costs. Normalization adjustments may also be made to owner/officer compensation to bring it in line with comparable companies.

In the case of an operating company with stable cash flow, in order to develop a reliable valuation the benefit stream (cash flow) would need to be adjusted for considerations such as:

Further adjustments to the discount rate would need to be made for risk considerations, including:

Adjustments also would be needed for growth considerations, such as:

The discounted future cash flow method is applied when a company’s future operations are expected to differ from the past. Possible situations are:

Management must be willing and able to provide projections to the business appraiser in order to apply this method.

As with all approaches to business valuation, the income approach has some drawbacks as well as advantages. On the pro side, the income approach:

On the con side, the income approach requires management’s input on cash flow, risk and growth, which can be subjective. Adjustments to cash flow are also required to normalize the benefit stream. It also requires adjustments to cash flow to normalize the benefit stream. Moreover, income estimates for a five-year period can be considered speculative and difficult to authenticate.

But even with these considerations, the income approach remains the most appropriate approach to business valuation for an operating company with positive cash flows.

In the world of business valuation, the market approach is often emphasized due to its reliance on market data to derive fair market value. This method examines transactions of similar companies to estimate the value of your business. The pricing multiples derived from these market transactions are applied to the subject company’s metrics to derive its relative value.

There are four commonly used methods within the market approach:

This method assesses the value of your company based on the stock prices of similar public companies. It’s most effective when there are publicly traded companies that share characteristics with your business.

These companies are ones that are traded on one of the publicly listed exchanges such as the NYSE, NASDAQ and American Stock Exchange. There are also other smaller exchanges including Chicago Board of Trade, Over the Counter, Bulletin Board and Pink Sheets.

The advantage lies in the accessibility of data through public filings like 10Ks and 10Qs. However, the challenge is finding a truly comparable public company, especially for smaller or niche businesses. A main street electronics store is not going to compare well to an Apple or NVIDIA stock.

The guideline transactions method relies on pricing multiples derived from transactions involving similar companies and applied to the subject’s metrics to determine the value of the subject interest. These transactions are found on databases such as BizComps, Institute of Business Appraisers, Done Deals, Factset Mergerstat, Capital IQ and DealStats (formerly Pratt’s Stats.) Each of these databases has information on tens of thousands of private company transactions.

In this method, market multiples are derived from the transactions of the companies and applied to the subject company. The advantages to this method are information for similar sized companies and specific industries are available. However, the information is limited to what is reported, and comparable transactions may not exist. The transactions reported in these databases generally lack adjustment: stock transaction values are provided without interest- bearing assets and liabilities and asset transaction values are provided without cash, receivables, prepaids, non-operating assets or liabilities. These items are added back to the calculation before the market value of implied capital amount is determined.

Note: Depending on the number of transactions and the reliability of those transactions, the market approach could be used as a sanity check in comparison to the income approach. Sometimes, when the guideline companies are not very good, or the number is not sufficient, the market approach is excluded entirely. There are certain NAICS or SIC codes for which no data is available. There are certain NAICS or SIC codes for which there is no data available. We see this commonly in the agriculture industry, since most of the transactions are closely held, related party transactions of legacy farms. These transactions are hardly reported.

When there are not applicable guideline transactions, either public or private, available for comparison, the past transactions method can be considered. However, this method is only applicable when the subject company has had previous arm’s length transactions. Transfers among family members or employees are generally not representative of fair market value. These transactions are provided by the internal management of the company or prior valuations performed by a certified analyst.

The final method within the market approach is the industry method, or rule of thumb method. This method is a simplified form of the market approach. A “ballpark” multiple is applied to the earnings of the subject company to determine the value of the business. This method is applied commonly by business brokers and can be applicable to main street stores.

The choice among these methods depends heavily on the size, industry and specific characteristics of your company. The goal is to find the most accurate and relevant comparison to determine your company’s fair market value.

The asset approach is the go-to approach for use in a business valuation that focuses on a company’s net asset value when there is very little to no goodwill or intangible assets to consider. The asset approach (or asset-based approach) is based on the premise that a company’s value can be derived from the total value of its underlying assets minus its liabilities. This method is particularly useful when valuing companies that are asset-intensive – such as farms and construction companies – or in cases where the business is being liquidated. It is also commonly used for holding companies, distressed businesses and businesses with a lack of income or cash flow that cannot be normalized.

Business entities with significant and, in many cases, valuable physical assets may not necessarily generate a large return on investment, making the income-based approach and the market-based approach inappropriate for valuation purposes. Farmland is one example where there is high capital appreciation in the value of the land. However, farm rents and income generation may not be particularly strong. So the highest indication of value on a farm or an entity that holds a lot of farmland will be reached with the asset-based approach.

Other asset-intensive businesses for which we often use the asset-based approach include construction companies, which own heavy machinery and have tight margins, depending on market conditions. In valuations of these types of companies, the owners must obtain a separate appraisal of their equipment to support the valuation.

Additionally, the asset-based approach is commonly used for distressed companies, those that are experiencing consistently low earnings or losses and which may be on the brink of being sold or liquidated.

The primary method within the asset approach is the adjusted net asset method.

The adjusted net asset method provides a more accurate reflection of the company’s value by adjusting the book values of assets and liabilities to their current fair market values. This method involves:

The practical application of the asset approach involves several steps:

Example: Consider a manufacturing company with substantial physical assets, including factories, machinery and inventory. By revaluing these assets to their current market value and subtracting outstanding liabilities, the asset approach can provide a clear picture of the company’s value independent of its income-generating capacity.

It’s important to note that the asset-based approach does not take into consideration any intangible assets such as goodwill. While intangible assets may be noted during the gathering of data, they are not accounted for in the final valuation.

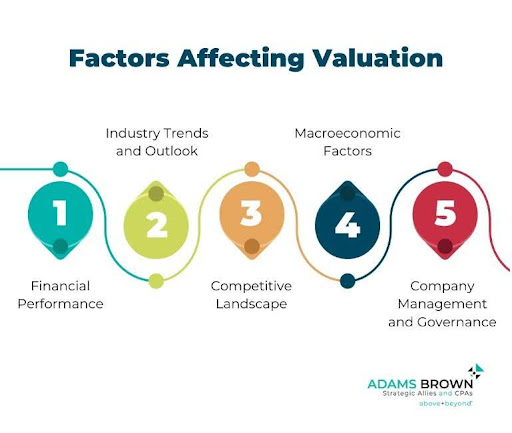

Business valuation is both a science and an art, rooted in financial data but heavily shaped by qualitative elements. One of the most direct influences on a company’s valuation is its financial performance—specifically revenue, profitability and cash flow. Consistent revenue growth and strong margins signal a healthy business, while reliable cash flow demonstrates the company’s ability to fund operations, service debt, and generate returns. Valuators often use these figures as the foundation for income-based valuation models such as discounted cash flow or capitalization of earnings.

Industry trends and the company’s risk profile also carry significant weight. A business operating in a fast-growing, innovative industry—like tech or renewable energy—typically commands higher multiples due to investor optimism and market momentum. In contrast, companies in declining or highly regulated sectors may face downward pressure on value due to uncertainty or limited growth prospects. Risk factors such as dependence on a single supplier, litigation exposure, or volatile earnings can further depress valuation.

Customer concentration and market share play a crucial role in assessing the stability of future earnings. A company that relies heavily on just one or two customers is exposed to heightened risk, which can lower its valuation. Conversely, a diversified customer base and strong market presence often lead to a more favorable outlook, as they suggest resilience and competitiveness.

The size of the business and its growth potential also shape valuation outcomes. Larger companies generally benefit from economies of scale, stronger infrastructure and broader access to capital. Businesses with clear paths to expansion—whether through new markets, products or services—are more attractive to buyers and investors, often leading to higher valuations.

Broader economic conditions, including inflation, interest rates, and GDP growth, can influence both buyer behavior and valuation methodologies. For instance, in a low-interest-rate environment, future cash flows are discounted less steeply, which tends to raise valuations. In contrast, economic uncertainty or tightening credit markets can dampen buyer enthusiasm and increase risk premiums.

Finally, the strength of a company’s leadership and internal operations can make or break a valuation. Experienced, stable management teams with a track record of execution inspire confidence in the business’s ability to meet future targets. Well-documented processes, scalable systems and strong governance also enhance value by reducing operational risks and ensuring continuity after a transition. In short, the more a business appears capable, predictable and positioned for growth, the higher its likely valuation.

Valuation multiples are tools used to translate a company’s financial performance into an estimate of its market value. Common multiples include EBITDA (earnings before interest, taxes, depreciation and amortization), SDE (seller’s discretionary earnings) and revenue. EBITDA multiples are most frequently used in mid-market and institutional transactions because they normalize earnings and remove non-operational noise, offering a clearer picture of operating performance. SDE is often applied to smaller, owner-operated businesses since it accounts for the total financial benefit available to a single full-time owner-operator. Revenue multiples are used when profitability data is inconsistent or unavailable, typically in early-stage or rapidly growing businesses. Each multiple is applied to the relevant metric to produce an enterprise value estimate, which is then adjusted based on working capital, debt and other specific factors.

Valuation multiples are not universal—they vary widely by industry, company size, growth prospects, customer concentration and risk profile. For example, a SaaS company with recurring revenue and strong margins may command a higher EBITDA or revenue multiple than a capital-intensive manufacturing firm. Industry benchmarks serve as a starting point, but adjustments are made based on factors like geographic reach, intellectual property, client diversification and regulatory environment. Professionals rely on databases, proprietary comps and published transaction data to determine what multiples are reasonable for a specific sector and scenario.

Comparable markets are selected by identifying recent transactions involving similar businesses in terms of size, industry, geography and financial performance. These comps are drawn from public deal databases, private transaction reports and industry analyses. Once a pool of relevant comps is established, valuation experts analyze the multiples paid in those deals and adjust them to reflect differences between the subject company and the comparable. The result is a refined range of multiples that, when applied to the company’s financials, produce a market-informed valuation estimate. This method helps ground the valuation in real-world buyer behavior and investor expectations.

Business valuations are highly specialized engagements that require a combination of financial acumen, industry knowledge and technical training. To ensure reliability, most credible valuations are conducted by professionals who hold specific credentials in the field. Among the most recognized designations are CPA/ABV (Certified Public Accountant/Accredited in Business Valuation), ASA (Accredited Senior Appraiser), CVA (Certified Valuation Analyst) and CBA (Certified Business Appraiser). Each of these credentials involves rigorous training, examinations and adherence to professional standards, and each comes with a commitment to ethical and defensible valuation practices.

Working with a credentialed valuation professional is essential, particularly when the valuation will be used in high-stakes situations such as litigation, IRS disputes, mergers and acquisitions, estate planning or divorce proceedings. Credentialed professionals are trained not only in the application of valuation methodologies but also in the regulatory, legal and tax implications of their conclusions. They know how to appropriately adjust for risk, apply valuation discounts, analyze financial statements and document assumptions in a way that can withstand scrutiny from courts, auditors and tax authorities.

Choosing the right valuation expert involves more than verifying credentials. Business owners should look for someone with relevant industry experience and a track record of similar engagements. It’s important to ask about their familiarity with businesses of similar size and structure, the purpose of the valuation (e.g., transaction, tax, dispute), and their process for reaching and documenting conclusions. Owners need someone with strong communication skills who can explain complex valuation concepts in a clear, practical manner. Finally, independence is key: the expert should be free of conflicts of interest and committed to providing an unbiased, well-supported opinion.

Ultimately, the credibility of a valuation hinges on the qualifications of the individual who prepares it. A well-credentialed, experienced valuator not only produces a more accurate result but also enhances the defensibility and usefulness of the valuation in any financial, legal or strategic context.

Business valuation plays a pivotal role in shaping a successful exit strategy. Rather than being a final step in the sale process, valuation should be integrated early to inform decision-making and drive strategic planning. It provides a realistic, market-based picture of what the business is worth, enabling owners to align their financial goals with the company’s current value and future potential. A thorough valuation reveals strengths and weaknesses that can either be leveraged or addressed prior to exit such as customer concentration, profitability or operational inefficiencies. This insight allows business owners to take proactive steps to enhance value over time, whether through cost control, revenue growth or improving the scalability of operations.

Timing the sale is equally critical. Business owners who obtain a valuation two to three years before they plan to exit are in a stronger position to time the market and optimize value. This window allows for strategic improvements that directly impact the valuation such as cleaning up financials, resolving outstanding legal issues, strengthening management teams or securing long-term contracts with key customers. Furthermore, aligning the timing of the sale with favorable economic, industry or company-specific trends can significantly improve the purchase price and the quality of buyer interest.

Valuation also plays a central role during the due diligence phase and in buyer negotiations. A well-prepared valuation report serves as a credible and objective foundation for the asking price. It establishes a clear narrative for how the value was determined and provides transparency into the methodologies used. This not only strengthens the seller’s negotiating leverage but also helps build trust with potential buyers. During due diligence, when buyers are scrutinizing financials, customer lists, contracts and compliance, a robust valuation can preemptively address questions, highlight justifications for adjustments and reduce the risk of price erosion or deal delays. Valuation is not just a number. It’s a strategic tool that enhances planning, supports negotiations and maximizes exit outcomes.

Buy-sell agreements are foundational documents for closely held businesses, especially those with multiple owners. These agreements dictate how ownership interests are transferred in the event of certain triggering events such as death, disability, retirement, or a voluntary exit. A clearly defined valuation method within the buy-sell agreement is essential because it ensures all parties have a mutual understanding of how the value of ownership interests will be calculated. Without a pre-established method, disagreements are almost inevitable, and disputes over price can lead to strained relationships, litigation, or even dissolution of the business.

Including a valuation method—whether it’s a fixed price updated annually, a formula based on earnings or revenue, or an independent third-party valuation—provides structure and predictability. Many agreements also designate specific valuation standards, such as fair market value or fair value, and whether discounts for lack of control or marketability should apply. The valuation method selected should reflect the realities of the business and be consistently applied.

Because business conditions change over time, it’s critical to update valuations periodically. If the buy-sell agreement uses a fixed value or formula, it should be reviewed and revised at least annually. If it calls for a third-party valuation, owners might opt to obtain a new appraisal every few years or immediately following a major change in the business. Triggering events such as the departure or death of an owner require that the valuation method be applied promptly and accurately, and any ambiguity at that stage can delay the transaction and increase the likelihood of conflict.

The best buy-sell agreements anticipate potential disagreements by documenting terms in detail. This includes how and when the valuation will occur, who will perform it, how disagreements between valuators will be resolved and what role discounts or premiums will play. By proactively addressing these issues, owners can ensure that transitions happen smoothly, preserve the financial health of the business and maintain harmony among shareholders or family members. Ultimately, a well-crafted valuation clause in a buy-sell agreement is about creating clarity, fairness and continuity before emotions or competing interests complicate the process.

Gift and estate planning has grown more complex in recent years, in large part due to a confluence of tax laws, demographic trends and market forces that are unusually volatile. As a result, valuation of assets for gift and estate planning purposes requires increasingly exacting methods used by valuation professionals and an understanding of changing tax laws and IRS practices.

Business valuations are an essential support tool for gift and estate planning. Most business owners have nearly all of their personal net worth tied up in their companies, a factor that can complicate estate planning. If the business is part of the estate, a valuation can be done before estate planning and gifting of assets and updated every couple of years to ensure that the plan is realistic.

In cases where a business owner is not planning to exit the company anytime soon, obtaining a valuation for estate planning purposes can deliver the double benefit of providing insight into the business’s value drivers and what steps can be taken to enhance the value over time.

On average, 350,000 business owners who are members of the baby-boom generation exit their businesses annually. Many of those businesses, including family farms, small businesses, manufacturers and local retailers, are included in gift and estate plans, as well as trusts. Structuring these plans and trusts to accomplish the owners’ goals while avoiding or minimizing estate taxes is a key goal for owners and their advisors.

But current volatility is leading many business owners and their advisors to review their estate plans and carefully consider how they may be restructured and how assets may be valued in the next couple of years. The volatility comes from several sources.

First, there is the Tax Cuts and Jobs Act of 2017 (TCJA), which significantly increased federal estate tax exclusions to the current $12.9 million for individuals and $25.8 million for married couples. But, like many other provisions of TCJA, the expanded estate tax exemption is scheduled to expire on Dec. 31, 2025. Unless Congress acts to extend or make permanent the current exemption, it will revert to pre-TCJA levels of approximately $5.5 million for individuals and $11 million for married taxpayers. Such a dramatic contraction of the federal estate tax exemption would push many taxpayers’ estates over the line, subjecting them to estate taxes unless they proactively restructure their estates before the change.

Second, market forces such as inflation and the rapid pace of business exit by baby boomer owners are impacting valuations, a situation that was compounded by the COVID-19 pandemic, which accelerated business exits.

Third, with additional funding from the Inflation Reduction Act of 2022, the IRS will be ramping up enforcement in the next few years potentially increasing IRS challenges to business valuations included in gift and estate plans.

Structuring an estate or gift plan to avoid estate taxes makes sense. The top tier estate tax rate is 40% for estates that are larger than $13.9 million for an individual. Depending on where you live, you may be subject to state-level estate taxes, as well. Kansas and Arkansas do not have estate or inheritance taxes, but Nebraska and Iowa do.

Valuations are a helpful tool in the gifting context as owners prepare for exit. A valuation enables wealth to transfer from one generation to the next in a tax-smart manner and satisfies the IRS’ requirement for adequate disclosure of assets. Once the IRS accepts a valuation report, it can still lodge a challenge within the next three years.

A valuation enables owners to transfer pieces of the business to heirs or other successors over several years, minimizing tax consequences while keeping the estate below the estate tax threshold.

In the event a trust is created to hold a business, beneficiaries are typically given nonvoting shares or a minority interest with restrictions on their ability to transfer the interest to someone else. In these cases, a valuation would reflect a discount for lack of control and lack of marketability. The IRS often challenges these discounts, so it’s important to work with a valuation professional who understands the best methods to use to be following the IRS’ standards.

Going into negotiations to sell a company can be a stressful and even emotional experience for a business owner. In some cases, they’ve built the company and come to the point that always seemed far in the future, the point of business exit.

One factor that can give a seller confidence going into merger and acquisition (M&A) negotiations is an independent business valuation performed by a valuation professional. A business valuation helps the seller set reasonable expectations as to the price they are likely to get for the business, and it provides detailed data and information that can help defend the price if negotiations become challenging.

Most importantly, the business valuation provides an understanding of what drives the value of the company, such as strong cash flow, a steady growth trendline and low risk factors. If the data shows that a company’s performance has declined in recent years, the valuation may provide context for the owner to decide whether to wait and go to market later or proceed with the sale now and try to get the best price possible.

People see risk differently, so the risk component of a business valuation is very subjective and may play a role in the negotiations between buyer and seller. It can be measured through the discount rate used in an income approach to business valuation and is implied in a reciprocal of the valuation multiple. (See more below about different approaches to valuation.)

The type of buyer you’re dealing with in a negotiation may have a significant impact on how the business valuation is perceived, with some buyers being more focused on cash flow and growth and others concerned with risk. In most cases, there are two types of buyers – internal and external.

Internal buyers may include a key person or several key managers who may already be running the business and want to stay with the company, and who have the resources to buy it. Internal buyers are going to be more familiar with the company’s strong points and weaknesses and may be able to negotiate a discount on the price.

External buyers include third-party buyers, competitors, private equity companies and other unrelated parties who are interested in owning the company. They may have very different reasons for wanting the company than internal buyers would, and they are generally willing to pay a higher price. For them, the synergistic value of the company may include enabling the buyer to expand their current business with a new product line or providing a key investment opportunity.

While cash flow, growth and risk factors are the primary drivers of a company’s valuation, several other elements can influence the price during M&A negotiations. For example, a potential buyer who is a competitor in the same industry may be willing to pay a premium for the customer lists, knowledgeable employees, processes and equipment that will come along with the acquisition. Those assets, among others, will influence the conclusion of value.

Ideally, a seller would go into negotiations with a potential buyer not only with a current business valuation, but with a benchmark valuation done several years earlier that will demonstrate the improvements that have been made to the business, as well as the resulting enhancement of value.

All stakeholders will want to ensure that the appropriate methods have been used to determine the value of a company. The most accepted business valuation methods and their advantages include:

At its most basic level, a business valuation is a process of determining the value of a business. There are three approaches to valuation, and all three should be considered as part of a comprehensive valuation process:

When preparing a valuation, all three approaches must be considered. The resulting values are evaluated to determine a final estimate of value using the best approach or combination of approaches.

However, different companies have different circumstances, and different industries lend themselves more to one type of approach than another. Consequently, a valuation professional must determine how much weight to give to each value. Sometimes equal weight is given to all three, and other times one methodology will be disregarded, with the value determined by the other two. For instance, the asset approach generally doesn’t make sense for a service-oriented business, since the value is in the services the business provides and not its equipment. But for a family farm, the asset approach will most likely rule because of the high value of land, which is often higher than the income being produced from it.

Business owners often seek valuations when they are considering selling their companies, but there are many other reasons to get a valuation. For example:

Estate planning is another strong reason for obtaining a business valuation. Whether the business will be passed to the next generation of family owners or sold as part of the estate, its value as a piece of the owner’s estate is an important factor.

Business valuations are typically performed by credentialed professionals such as CPAs with the ABV (Accredited in Business Valuation) credentials, CVAs (Certified Valuation Analysts), ASAs (Accredited Senior Appraisers) or CBAs (Certified Business Appraisers). Working with professionals, like those at Adams Brown CPAs, ensures that the valuation meets industry standards, withstands scrutiny and complies with IRS and legal expectations if required.

The valuation process starts with an in-depth review of the company’s financial records, operations and industry position. A valuation expert will typically use one or more of the three main approaches: the income approach, which looks at future earnings potential; the market approach, which compares your business to similar companies that have been sold; and the asset approach, which is based on the net asset value of the business. The chosen method depends on the nature of the business, its industry and the purpose of the valuation.

To produce a comprehensive business valuation that is more than numbers – a valuation that tells the story of your business – a valuation professional will interview you and your key managers to learn about your business and what makes it operate efficiently.

The valuation professional will also learn about your industry, your customer base, how you do business and whether you are operating in a high-risk or low-risk environment.

Before you call a valuation professional:

The documentation the valuation professional will need includes:

The documentation list may seem overwhelming, but it helps establish important information and intangible factors that impact valuation, such as risk.

Rule of thumb: Goodwill is the “how” a company performs daily operations. It’s an intangible asset, often resembling the “opportunity” identified by a prospective buyer. Common examples of goodwill include:

The impact of goodwill on a company’s valuation can be significant.

For example: Say a company is valued at $10 million. The real estate, equipment and the working capital are valued separately at $6 million, leaving $4 million allocated to goodwill. In other words, 40% of the company’s value is comprised of goodwill.

Note: This is an example, and the value of goodwill will vary depending on factors including the specific buyer, deal structure and terms of the deal, etc.

Not only can goodwill represent a significant portion of company value, but it’s often a key factor in a company receiving a premium or a discount on its sale price. Or, in other words, price multiples. For example, assume the sale of two companies in the same industry, and of similar size (in terms of revenues). But Company A sells at a seven multiple and Company B sells at a five multiple. Why is there a difference? Probably because Company A has better profitability. But why? Large in part due to goodwill – Company A exhibits:

It’s very likely that Company A is going to show stronger financial performance. This, plus the strength of their goodwill, is going to fetch a higher valuation.

Valuing the Company to determine the estimated goodwill is also a great KPI when measuring a company’s financial performance. We often use market multiples as a strategic planning tool. For example, if a company is valued at a multiple of 6x EBITDA, then in theory, every $1 of incremental EBITDA will result in $6 of incremental value. Pretty simple, until you put it into practice – does this mean revamping operations to improve efficiencies and margins? Does this mean better training to improve your people? Or investing in key employees? Many, many ways exist to drive value. But understanding your Company’s value to measure goodwill is best practice.

Enterprise goodwill is the value generated from some of the factors mentioned above that are owned by the business. Note: Not to be confused with intellectual property. It focuses on the value owned by the company, as opposed to the individual.

Alternatively, personal goodwill is value owned by an individual that either owns or is employed by a company. It is more common within companies that require specific credentials, experience and qualifications (e.g., dental practices, professional service organizations, general contractors, owner/operated companies, etc.) but is also in present in the form of customer relationships, key employees (sales, operations, etc.) or specialized knowledge/skills held by an employee.

When determining the nature of goodwill (enterprise vs. personal), a good rule of thumb is to ask yourself – “If this person were to leave the business, what would happen?”

Why is this important? Personal goodwill has very little, if any, value in the eyes of the buyer, and more importantly, lending institutions, insurance and any other stakeholder with a financial interest in the sale of the company. And for obvious reasons, why would a company pay for value that cannot be transferred into the business?

And to clarify, the presence of personal goodwill, regardless of the form, is not a “deal killer.” And in many cases, it won’t dilute the value of a company, so long as there is an agreed upon plan in place for the transition of personal goodwill into enterprise goodwill. Predominantly in the form of an earnout, i.e., a specified amount of time (months, years, etc.) that the owners of a company are contractually obligated to assist with the transition of ownership after the sale.

Yes. The firm provides valuation services for use in estate, gift and income tax planning purposes.

Yes. Adams Brown offers business valuation services to help business owners and shareholders with mergers, acquisitions, sales and spin-offs.

Complete the form to the right to start a conversation with our business valuation team.