When Should your International Exporting Business Consider an IC-DISC?

How this Tax Strategy Benefits Manufacturing Companies

Key Takeaways:

- The IC-DISC structure offers significant tax benefits for U.S.-based manufacturing businesses involved in international exporting by reducing their taxable income and allowing profits to be taxed as qualified dividends.

- Establishing an IC-DISC involves specific steps and compliance requirements, including filing Form 4876-A, meeting gross receipts and asset tests and maintaining separate books and records.

- Despite changes from the Tax Cuts and Jobs Act, the IC-DISC remains a valuable tax strategy for pass-through entities, with potential benefits especially pronounced if future tax rates increase.

If your U.S.-based manufacturing business engages in international exporting, you may benefit from a tax structure known as an Interest-Charge Domestic International Sales Corporation (IC-DISC).

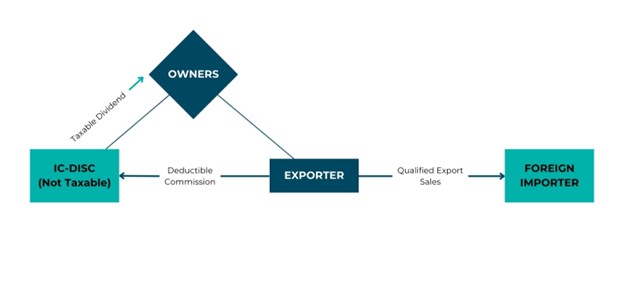

Enacted by Congress in 1971, the Domestic International Sales Corporation (DISC) was designed to help U.S. exporters even the playing field by reducing the U.S. tax impact, thereby supporting economic growth. This separate legal entity is a tax-exempt C Corporation which provides services to a related U.S. exporter for a fee. It has no activity aside from a commission received from the exporting entity and the payout of qualified dividends to owners. Any organization with exporting activities can consider this structure.

How Does it Work?

The IC-DISC entity and exporting entity operate in a brother-sister relationship. Here’s a simplified breakdown of the process:

- Commission Payments: The exporting entity pays a commission to the IC-DISC.

- Tax Deduction: This commission is deductible for the exporting entity, reducing its taxable income.

- Tax-Exempt Status: As a tax-exempt entity, the IC-DISC’s profits are not subject to corporate tax.

- Qualified Dividends: These profits are only taxed when paid out as qualified dividends to the owners, who typically share the same ownership structure as the exporting entity.

Implementing an IC-DISC & Filing Requirements

Setting up and maintaining an IC-DISC is relatively straightforward. Here are the key steps and requirements:

- The corporation is organized under state law.

- The IC-DISC election is made via Form 4876-A within 90 days after the intended beginning of its tax year.

- On an annual basis, a newly created IC DISC corporation must meet the following tests, per the IRS:

- At least 95% of its gross receipts during the tax year are qualified export receipts (QREs)

- At the end of the tax year, the adjusted basis of its qualified export assets is at least 95% of the sum of the adjusted basis of its assets.

- It has only one class of stock and its outstanding stock has a par or stated value of at least $2,500 on each day of the tax year.

- It maintains separate books and records for the entity.

- Its tax year must conform to the tax year of the principal shareholder who has the highest percentage of voting power.

- Its election to be treated as an IC-DISC is in effect for the tax year.

- This newly created entity has an annual tax filing requirement via Form 1120-IC-DISC. It is due by the 15th day of the 9th month after the entity’s tax year ends. There are no extensions for this filing.

Questions?

While the Tax Cuts and Jobs Act (TCJA) of 2017 reduced the impact of the IC-DISC as a tax planning strategy by lowering corporate tax rates from over 35% to 21%, it remains a valuable tool, particularly for pass-through entities. The current qualified dividend max tax rate is 20% + 3.8% Net Investment Income tax. As a result, this “shift” of funds for an exporter entity structured as a C Corporation is not as fruitful as it once was. From a pass-through entity perspective, it makes more sense under current tax law. The highest marginal individual income tax rate is currently 37%.

Therefore, an exporting entity under this structure can reap more of the associated tax benefits. As we are currently in an era of historically low tax rates, utilizing an IC-DISC can be a powerful strategy, especially if tax rates increase in the future. Contact an Adams Brown manufacturing advisor for more information regarding this tax strategy.